Coin bank satirizing Boss Tweed and Tammany Hall (1873) | American History Museum / CC0

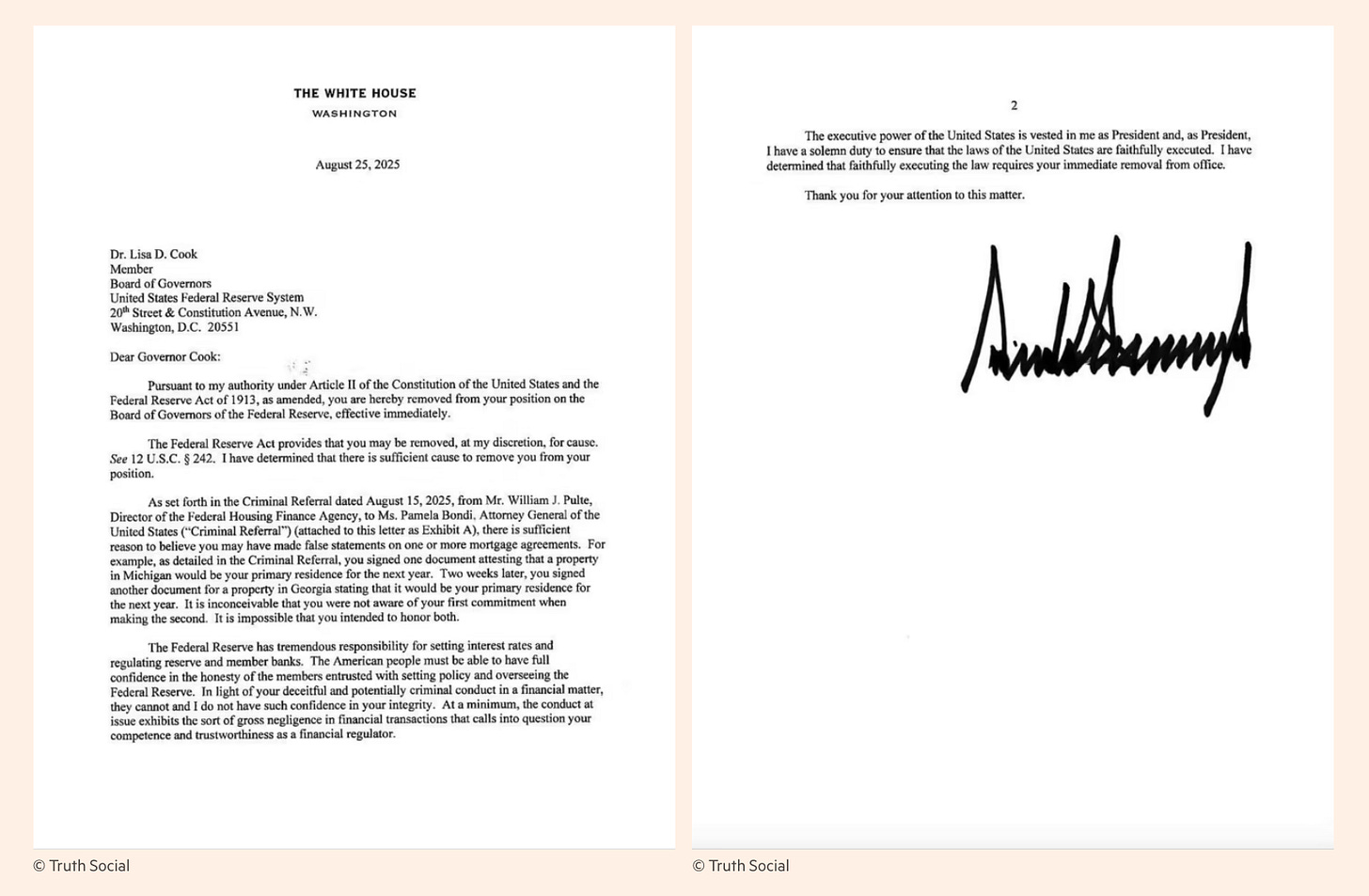

Donald Trump’s move to fire Fed Governor Lisa Cook “for cause,” escalates his long-running battle with America’s central bank.

The news has triggered outrage. In the pages of the FT, David Wessel, director of the Hutchins Center for Fiscal and Monetary Policy at the Brookings Institution, warned: “President Trump seems determined to control the Fed—and will use any lever he has to get a majority on the Federal Reserve Board of Governors,” he said. “This is one more way in which the president is undermining the foundations of our democracy.”

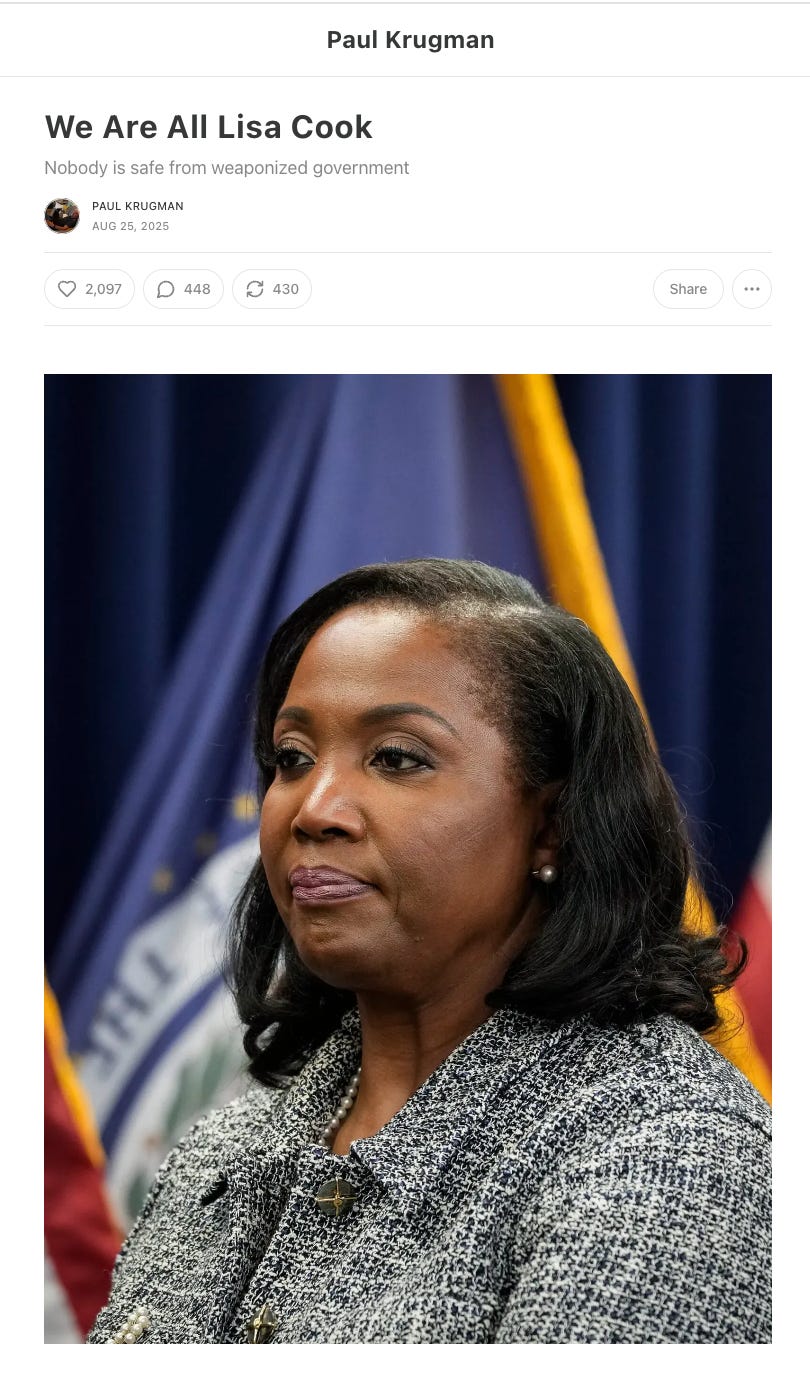

If Wessel’s “our democracy” was a resonant phrase, Paul Krugman went one better:

And, never one to hold back, Krugman ended his rallying cry with “I’m Spartacus!”

Now Trump’s moves are out of the ordinary. They escalate his long-running feud not only with the Fed but the administrative state in general.

In May, in ruling on Trump’s firing of officials at the National Labor Relations Board, the Supreme Court was at pains to insist that “the Federal Reserve is a uniquely structured, quasi-private entity that follows in the distinct historical tradition of the First and Second Banks of the United States.” The President cannot, therefore, simply fire the Chair or Governors without cause. There is, however, an untested clause in the Federal Reserve Act of 1913, which allows the chair or Governors to be fired for “cause.” And since May, the Trump camp seem to have been on the hunt for “causes.” First there were the construction costs of the Fed renovation. Now there is Cook’s mortgage application.

One interesting line is to enquire why the Trump side is escalating so hard and so fast. After all, the Fed is coming around to making rate cuts. They are going to get what they want. Why are they forcing the pace?

Is it opportunism? They found some dirt and they are going to use it. Is it a matter of MAGA hubris and control-freakery? They are determined to break the Fed as an independent institution. Is this about the long-game on banking regulation? Or are they genuinely concerned about the state of the US economy and are they thus determined to get control of Fed policy so that they can launch a major stimulus in 2026 ahead of the mid-terms?

But pause for a second to consider the liberal reaction. It too is telling. Consider the personal identification that is invoked here. “OUR democracy.” “I’m Spartacus!”

At one level it is silly. At another it is painfully true.

It is silly because the Fed is a very undemocratic institution. One of the reasons that the balance on the Fed board matters so much is that next year the regional Fed chairs are up for appointment. In picking regional chairs, the Fed in Washington oversees what is otherwise unaccountable and opaque affairs dominated by local committees of business interests. The Fed is one branch of US government where business is directly represented in power. Ponder that for a minute, “I’m Spartacus!”

People inside that system have power. Lisa Cook isn’t just a person like you and me, with views that diverge from Trump’s. She is a Federal Reserve Governor. She has a vote on one of the most important decision-making committees in the world. Krugman doesn’t. I don’t. We don’t. We are NOT all Lisa Cook.

But strip away the outraged and outrageous generality of the claims, and all of a sudden, you see something painfully true.

Lisa Cook is a classic instance of a successful, competent Professional Managerial type, at least that is how she struck me when I had the privilege of serving on a committee with her. She is “one of us.” In that restricted sense Krugman is not wrong. Anyone who exercises some degree of authority and control in the PMC mode—and that probably includes a fair share of the folks reading this newsletter or Krugman’s—is at least somewhat vulnerable to the kind of harassing attack she is suffering. And we should know. After all ethics, reporting, disclosure are very much our stock in trade.

As far as this more restrictive “we” is concerned, Wessel isn’t wrong either. If by “our democracy,” we mean the Brookings-Institution-kind-of-democracy, then yes: The pillars of “our democracy” in that sense are very much under threat.

MAGA 2.0 clearly does want to challenge “our” authority and redefine how “our” American democracy functions. They also want to do a bunch of much more blatant stuff about redistricting, vote manipulation, et cetera, but that is another story.

But rather than merely reacting with horror, this should give us pause. This is yet another moment that brings to mind Barack Obama[‘s] indignant but oh-so-telling riff : “Imagine if I had done *ANY* of this.” Well yes! Imagine …

Why were Democratic administrations not as ambitious, determined, ruthless, aggressive, risk-taking, not to say brave, in pursuit of our agenda as MAGA are in pursuit of theirs? MAGA may be bonkers and foolhardy. But they are willing to take risks in a way “we” were not. “Our democracy” may have been competent, but it was also conformist.

The committee that I was on with Lisa Cook was about green energy transition and finance. It also included ex–Fed Board member Sarah Bloom Raskin. In 2022, she was nominated for a top regulatory position at the Fed. She withdrew after scandal-mongering by Republicans and opposition over her position on climate politics from West Virginia senator Manchin. It was an incident that was highly indicative of the way in which constraints operate asymmetrically in US democracy. The Republicans were utterly ruthless and Manchin, an all-but Republican, held the whip hand. Of course, the Democrats aren’t innocents. They engage in lawfare on other fronts but not with regard to finance. That is the serious stuff. Hugely elaborate justifications had to be constructed to argue that it was appropriate for central bankers to engage with the green energy transition. In the US, it was always clear that none of them had much chance of success. Manchin put the nail in the coffin. And was there no dirt on Manchin? Really, none at all? Nothing to move the roadblock that he presented at a critical moment?

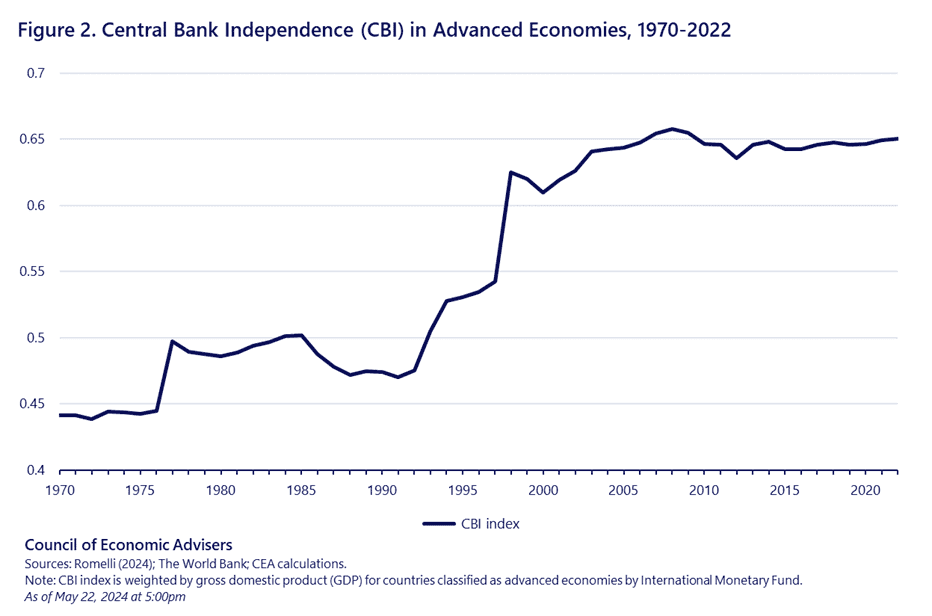

And then there were the economic arguments. As far as the Fed was concerned, MMT was anathema, and direct politicization was wrong because “economics showed us that independent central banks are better.” And those arguments are being mobilized again today. Bloomberg, tellingly, quoted a primer from Biden’s Council of Economic Advisors published in May 2024 on the importance of an independent Fed.

Here is an excerpt:

The Biden-Harris administration has consistently elevated the importance of an independent central bank. Given that this issue has come up in various settings, CEA thought this was a good moment to explain what central bank independence (CBI) is and why it is so important. An independent central bank is one that can carry out monetary policy without political interference. … Figure 2 shows that CBI has become much more prevalent among advanced economies.

Empirical evidence shows the evolution toward central bank independence has coincided with a long-term decline in inflation in advanced economies and corresponds to well-anchored long-term expectations.[4] Because of these macroeconomic benefits, governments around the world continue to increase central bank independence: a study of 370 central bank reforms from 1923 to 2023 finds a renewed global commitment to central bank independence since 2016. We in the Biden administration are highly motivated by this history and will continue our unwavering support for CBI. History could not be clearer regarding the lasting and damaging inflationary consequences of ignoring this lesson or reversing the hard-earned progress of the past half century.

Don’t expect such arguments to cut much ice with the MAGA crowd.

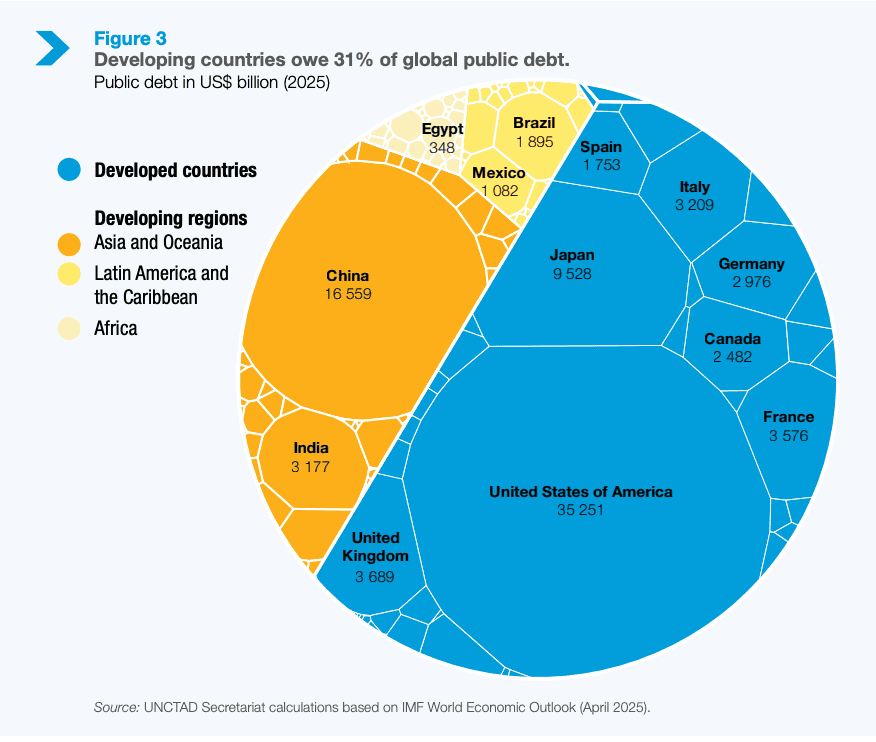

Again, you could say that MAGA are bonkers and foolhardy. But you might also argue that they have a point worth testing. Conclusions about the general advantages of independent central banks are derived from panels of countries that are far less significant to the world economy and have less capacity to set the terms. The US is the whale in the bathtub. It sets the terms for everyone else and nowhere more so than in finance. It enjoys “exorbitant privileges.”

You can say that undermining the Fed’s independence, risks undermining the position of the US at the heart of the global currency system. That may well be true. But where exactly are major investors to go? This is the universe of public debt available for investment worldwide.

If you want to invest trillions, your options, other than the US, are China or Japan, or a smattering of smaller European borrowers. It isn’t by accident that the Euro is riding high right now. But the Euro is far from being in a position to replace the mighty US Treasury market.

So far the markets have reacted calmly. As of the time of writing on Tuesday morning European time: “The 30-year Treasury bond yield—where most of the pain would probably fall if Trump succeeds in taking over the Fed—has climbed to 4.94 per cent this morning. That’s up from 4.75 per cent earlier this month, but still below the 5 per cent mark we last breached in May and October 2023.”

Can that last?

The brilliant Robin Wigglesworth at FT Alphaville starts his piece this morning with the words: “On the assumption that a chaotic, incoherent trade war was baked in the cake, FT Alphaville’s main bet for a financial-economic calamity under Trump 2.0 has long been that he launches a full assault on the Fed. Well, it’s here now.”

The piece is titled “Pray for the US Treasury market.” But what exactly is Wigglesworth asking us to pray for?

Are we praying for the US Treasury market to come through this episode without meltdown? Or are we praying for the bond vigilantes to come riding over the hill to discipline Trump? In which case we are praying for a crisis. Or are we praying for the Treasury market’s own soul. Are we praying that it has not gone over to MAGA madness? So far, the worry seems to be that the markets have responded hardly at all.

As Wigglesworth remarks:

The initial market reaction looks preposterously sanguine, given that this move cannot be seen in isolation. It was just weeks ago that president Trump sacked the head of the Bureau of Labor Statistics after an unflattering jobs report. Entrenched expectations of norms and institutional integrity are now kaput. Many investors have drawn comfort from the argument that any forceful attempts to take over and reshape the Federal Reserve would trigger a bond market hissy fit that even the Trump administration has shown a fear of. However, the nakedly political move against Cook shows that it is not nearly as worried about the market fallout as investors have assumed. Even if Cook were to eventually prevail through the courts, her hounding shows to everyone else on the Fed board that the Trump administration is gleefully willing to unleash its full clownshow on anyone that displeases them. That could easily have a pernicious impact on the central bank’s policymakers. They wouldn’t be human if they didn’t worry about a weaponised US government using all its available tools to harass them.

I’ve long been of the view that a more democratic politics of central banking and public debt, is the better alternative.

In light of the toxicity of American politics in general, that has always been a risky position. The other side are dangerous. If you open up the political game, you had better be sure that you can win it. The shutting down of the candidacy of someone like Sarah Bloom Raskin is indicative of how limited the room for maneuver is.

In the current situation, the aggression of the MAGA side, surely leaves us no option. History is forcing our hand.

Wigglesworth concludes his report with a great quote from Rabobank.

As Rabobank said: The unabashed politicization of the supposedly independent and technocratic process of setting the price of money once again confirms that it is no longer the 1990s and that old ideas about optimal policy transmission, central bank credibility and the need to insulate important decisions from the influence of the popular will offers little protection against the new paradigm of raw power politics. Just as the interpretation of law is inherently political, the price of money is inherently political, and all aspects of national policy are being co-opted to support the MAGA vision of the United States and its place in the world.

If Brookings-democracy belongs to the past. If the rolling assault on “us,” the PMC can no longer come as a shock but has to be taken as a given, then the question is: Is our reaction going to be defensive? Is the best that we can hope for some intervention by the Supreme Court, or a bond market panic? Are we going to retreat—in the name of Spartacus!—to a defense of central bank independence?

Isn’t it time to actually define what the appeal of “our democracy” actually is? Isn’t it time to define what a democratic politics of central banking might look like?

This essay was first published in Chartbook, the author’s newsletter, on August 26, 2025. Reprinted with permission.

Business interests advance boldly because they do not depend on outrage or numbers but on concentrated means and direct access to levers of power. A small minority with resources can cut through rhetoric and mobilization, bypassing the need to stir crowds or build moral cases. By contrast, Democrats, with mass support at their disposal, fall back on outrage, protest, and appeals to conscience. The asymmetry is stark: Roe is overturned, the military budget sails past one trillion, and genocide is funded while the base marches in the streets. Meanwhile, the managerial class keeps the machinery humming, allergic to principle. And so of course, what will Krugman do but shout fiery indignation from the comfort of his air conditioned office?