It is a widespread tendency to attribute financial volatility and economic crises in the global South to national policy makers. Despite the undeniable impact of policy choices and regulations on financial calamities, attributing the cause of economic breakdowns simply to the corrupt nature of political regimes, exclusionary institutions, or authoritarian statesmanship lacks insight into the political economic transformations within these countries. Commentaries on Turkey’s 2018-19 economic crisis were no exception in that sense.

For many observers, it is the authoritarian shift and the irresponsible policies accompanying the regime change of 2017-18 that led to the latest economic crisis in Turkey. They generally tend to deem the 2003-07 period as the golden years of the Turkish economy, despite the fact that Turkey’s credit-led model of accumulation was consolidated during this period. This model came to an effective end by spring 2018. It is this model of economic development, and not the latest shift in authoritarian techniques, that is to blame for the most recent crisis.

The 2018-19 crisis of Turkey is the latest crisis in the post-1989 period, i.e. the aftermath of liberalization of capital movements in Turkey. Concurrent with a series of financial crises in the developing world, Turkey witnessed financial instability and collapse periods in 1994, 1999, 2001, 2008-09. The latest crisis seems to be particularly important for Turkish pundits because it seemed to follow “the rise of authoritarianism” and the transition to the presidential system after the 2017 referendum and 2018 elections. Strongman politics, portrayal of the leader as the savior, and rule by decree in which the leader has the final word, are the basic elements of the new regime in Turkey. This, however, is not authoritarianism built from scratch, since Turkey had an authoritarian state form for the last four decades. What has been labeled as the authoritarian shift in recent years is rather “a shift in the predominant authoritarian technique,” to a more discretionary one such as rule by presidential decrees, almost completely bypassing parliamentary mechanisms.

Of course, there is no one-way relationship between new forms of political regime, populist authoritarian practices, and economic growth. It’s always complicated and mediated by a set of factors extending from global financial conditions to the domestic levels of private and public debt and the access of the domestic and newly internationalized capital to export markets as much as cheap sources of financing. Debtfarism, the imposition of increased forms of financial discipline upon the working classes, unemployed and the underemployed masses, dovetails with the authoritarianism of the AKP’s rule. Simply put, the direction of causality in the “authoritarianism à crisis” argument, made by not only many commentators but also scholars , is wrong, it’s more complicated than that.

I claim that authoritarianism was not the root cause of the 2018-19 crisis but that, being supported by debtfarism, it definitely had an impact upon the timing and the form the crisis took. Turkey’s dependency on capital inflows made the economy particularly vulnerable to changes in global financial conditions in recent years. I will briefly elaborate the handling of the 2018-19 crisis and contend that, until mid-2019, the AKP could not succeed in renewing debtfarism as it planned and the future of Erdoğan’s rule depends on success in this field.

The roots of the 2018-19 crisis

The roots of the latest crisis in Turkey can be traced back to the 2001 crisis and the reforms that followed. Unlike, say, Argentina, Turkey was the poster child for international financial institutions in the first couple of years after the 2001 crisis. Policy makers consolidated the banking sector and took steps for ensuring fiscal discipline. Interest rates declined and huge foreign direct investments followed suit. Despite the 2008-09 collapse, as the international financial crisis hit Turkey hard, the economy was back on track again in 2010 with the highest levels of monthly inflows and dramatic credit expansion. Household indebtedness ratio reached from well below 2 percent of the GDP in 2002 to over 18 percent of the GDP in 2013. Increased consumption capacity of the masses via the accumulated debt was crucial in the alleged success of the Turkish economy under AKP rule.

Debtfarism promotes reliance on expensive consumer loans to meet basic needs on the one hand and reflects the search of capitalists to benefit from formalized financial abstractions (such as interest rate as service fee, late fee as a penalty against overriding financial rules) to submit larger segments of society to financial discipline on the other. It is harder to object to service fees and commissions while real wages stagnate and access to basic services demands more money. Debt to disposable income ratio of households exceeded 50 percent in the early 2010s and were rolling over their debt thanks to interest rates lower than previous years. Debtfarism may increase the consumption capacity while normalizing the tensions of credit-led accumulation for a while. However, since credit is a gamble on future revenue flows, it is always susceptible to failure. Higher interest rates in the countries of the Global South, amidst tight financial conditions, make it harder for policy makers to renew debtfarism strategies and benefit from the financial discipline they impose.

Continuous capital inflows were necessary not only to support Turkish growth but also to lower the domestic interest rates in order to further stimulate domestic demand and keep political support. In the case of Turkey’s debtfarism, the weak chain was this dependency on foreign inflows. Therefore the policy makers responded to the 2008-09 crisis with an attempt to diversify the sources of finance, with the hopes of turning Istanbul into a financial center in the medium-term. With the benefit of hindsight, we can now safely claim that this endeavor failed.

The last decade saw a tremendous rise in foreign exchange (FX) borrowing in Turkey, particularly from 2009 to 2013. Turkish banks also borrowed cheaply to fund Turkish private sector’s appetite for foreign currency funds. By 2013, it became clear that any tightening of the global financial conditions would lead to a dramatic collapse of the economy. Indeed, the forthcoming interest rate hikes in the Global North meant that the post-2013 world was increasingly crisis-prone for the countries of the Global South. Since the economies with higher current account deficit ratios and FX-denominated debt would be particularly hit, tightening of financial conditions raised eyebrows of those who were monitoring the Turkish economy.

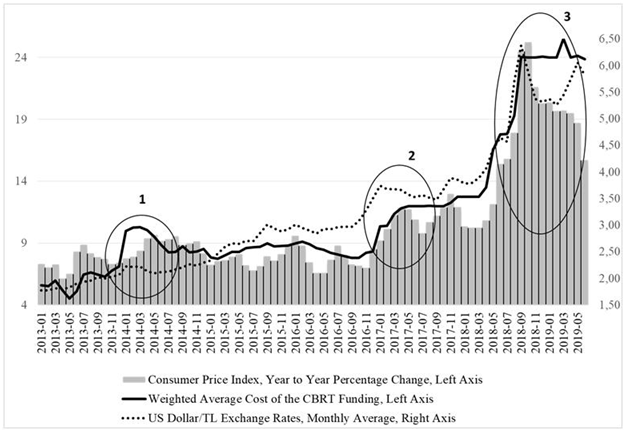

The Central Bank had to increase interest rates sharply, three times since 2013, to avoid further depreciation of Turkish Lira. Areas marked in the figure below show the continuous attempt to overcome the bottlenecks in Turkey, each time aggravating the situation as further depreciation could only be avoided by sharp interest rate hikes. These hikes were then followed by state-sponsored credit expansion periods to make debtfarism work once again, which would for the AKP cadres serve keeping the political power. Increasing interest rates to avoid sudden depreciation of the Turkish Lira (as seen in both early 2014 and 2016 autumn) was critical for keeping the inflow of financial capital. The state also sponsored a credit expansion by using state-owned banks (from late 2016 to mid-2017 and then once again in early 2018) and credit campaigns, and thereby managed to postpone the Turkish crisis amidst rising interest rates.

The management of the crisis: Did debtfarism work?

Turkish industrial investment under AKP governments did not yield any substantial technological transformation so as to make higher-value added goods occupy a more notable share in exports. Under these circumstances, the small and medium enterprises financially grew dependent on the state and the volatile growth of the economy relied on increased household consumption and hence lower interest rates. However, it was increasingly hard if not impossible to keep the debtfarism under tighter global financial conditions. Thus, it is not authoritarianism per se, but the contradictions of the credit-led accumulation that explains Turkey’s 2018-19 crisis.

Turkey’s currency crisis paved the way for a credit crisis in late summer and autumn of 2018. The responses to the 2018-19 crisis confirm that the policy makers wanted to see renewed credit expansion and searched for a way to make Turkish debtfarism work once again. However, the immediate response was to raise the interest rate 650 basis points (see figure above, area #3) in September. Despite the unwillingness of the AKP cadres, to avoid further foreign capital outflows and domestic capital flight, the Central Bank had no option but to raise the policy interest rate.

It became harder to renew credit expansion. At first sight, Turkey seemed to give up, with a renewal of debtfarism that worked several times before the 2018-19 crisis. The announcement of the New Economic Program (NEP) in September 2018 confirmed the commitment of the policy makers to a classical austerity program, which formed the first of three major responses during the crisis. The NEP foresaw mediocre growth rates for 2019 and 2020 and marketed them as the rebalancing of the economy. Not only providing fiscal discipline but also further strengthening market finance and reforming labor market, according to the NEP, Turkey would continue to be attractive for investors. The Program also suggested that, notwithstanding the radical decline in gross capital formation, the Turkish economy would harness this period for a renewed advance in the following years.

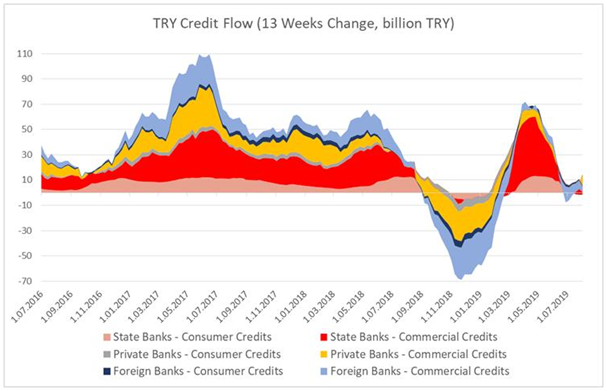

The second response was to work out the restructuring of the heavy debt of the private sector (real estate and energy corporations sitting at the top of the long list) forcing banks and corporations to negotiate. While bad debts kept increasing in late 2018, Turkish banks were able to restructure 20 billion USD worth of loans, and expected to restructure more in 2019. This response can be perceived as an element of the state sponsored credit expansion of late 2018 and early 2019, which helped many SMEs once again, before the upcoming local elections in March 2019. The AKP also used the Ziraat Bank (Turkey’s biggest state-owned commercial bank) and relied on other state banks to restructure household debt. Figure below shows the impact of the state-sponsored campaign of early 2019 on credit volume, and also the impact of those campaigns from late 2016 to mid-2017 and then once again in early 2018.

Last but not least, the third policy response has been the reduction of taxes in many sectors. While trying to contain the spillover effect of currency crisis before local elections, policy makers also attempted to stimulate the domestic market as fast as they could. This final element was the underlying factor in boosting state expenditure in the aftermath of the 2018 credit crunch. Ironically enough, increased consumption by the state avoided further contraction of the economy, while undermining the policy credibility of the AKP. The fiscal consolidation declared in the NEP was gone. The 12-month sum of the budget deficit reached the highest nominal level of the country’s history in May 2019. Since Turkey’s credit-led accumulation model depends on access to cheap sources of financing, kick-starting credit expansion repeatedly against the background of tighter global financial conditions, maintains, if not increases, the vulnerability of the economy. As a matter of fact the credit campaigns in 2019 against the backdrop of the geopolitical scandals the AKP has been a disruptive part of, made it only clear for many residents that new currency crises are forthcoming. Turkish residents kept hoarding American dollars, increasing the FX deposits in Turkish banks, also to the highest level in the history of the country in July 2019.

Given its mobilizing the state-owned banks for a renewed credit expansion, increased state expenditures, organization of commercial credit campaigns and its providing opportunities to households for rolling over debt it became clear ahead of the 2019 local elections that the AKP, despite rhetorical opposition for quite a while, was up for renewing debtfarism to overcome crisis. This was critical to maintain the support base of the ruling bloc, both small businesses and the society at large. The strategy did not work as expected, and in fact helped the political opposition to gain an electoral victory in the latest Istanbul elections.

Turkish authoritarianism and recurrent crises

The shift in the predominant authoritarian technique of the AKP required popular support, garnered only after the abortive coup in 2016. Like the AKP’s 17-year rule, it depended on and benefited from the expanding consumption capacity of the laboring classes and from keeping the social support base in general via strategies of debtfarism.

Tighter global financial conditions, domestic capital flight and the currency crises led to the blow of credit-led accumulation model in Turkey. The new one man regime and the rule by decrees, reminding one of Latin American caudillismo and having the capacity of being a precursor to something much worse, aggravated the situation and seemingly lengthened the duration of the crisis. But it was the accumulation regime itself that paved the road for 2018-19 crisis. Turkey’s authoritarian mode of incorporation of the laboring masses and the credit-led accumulation had been consolidated in the 21st century, reinforcing each other in due course.

Capital inflows and their pace have dramatically impacted the tempo of economic growth in Turkey in the last three decades. Credit-led model of accumulation gave the AKP its strength, but it faced surmounting troubles after 2013. The Turkish economy drifted into crisis in slow motion and the timing and severity of the crisis was partly shaped by the AKP’s attempts to postpone it. There is no one-way causality between authoritarianism and economic crises. However, the power of credit was effective in consolidating authoritarianism in Turkey under AKP, and it worked to undermine the very capacity of the new regime under new conditions.

Ali Rıza Güngen is a political scientist and CHR/Carnegie Mellon University Distance Fellow. He is an executive board member of Turkish Social Sciences Association and a member of the editorial board of social sciences journal Praksis. Banned from working in Turkish universities with a statutory decree, he works independently on financialization in the Global South, debt management and financial inclusion in Turkey. He is the co-author of the 2014 book Financialization, Debt Crisis and Collapse (in Turkish) and co-editor of the 2019 book The Political Economy of Financial Transformation in Turkey. His articles have appeared in The Journal of Peasant Studies and New Political Economy.