No one can escape discussions about the state of “the economy.” They inform political campaigns in the U.S., debt and austerity battles in the Eurozone, and development efforts in the poorest countries in the world. Our ideas about “the economy” — how it works, what it involves, and how it is measured — provide the departure point for our debates over inequality, unemployment, wages and a host of other hot topics. And no metric for describing and assessing national economic health is used more frequently today than Gross Domestic Product (GDP).

GDP purports to measure the total value of all goods and services produced in a country over a specific time period. But there are serious reasons to question whether this metric, as currently calculated, properly measures the size of the economy.

While the term GDP and the modern system of national accounting designed to produce it date back only to the 1930s, estimates of national income have been carried out as far back as the seventeenth century. From the outset, efforts to measure the economy were intertwined with attempts to change or reform it. Normative ideals about “the economy” informed national accountants’ choices about what they included in their estimations. In his path breaking work Political Arithmetick (1665), Sir William Petty used his estimates of England’s national income to argue for a program of proportional taxation (where each taxpayer pays the same rate regardless of his/her income), asserting it would increase rather than decrease a nation’s (common) wealth. Over a century later, British Prime Minister William Pitt removed labor income from his estimation of national income because he sought to exempt labor income from taxation. And when John Maynard Keynes advocated compulsory savings as a means of funding World War II, his arguments rested upon the expenditure aggregate of consumption, investment, government spending and net exports that we learned in Econ 101: GDP = C+I+G+(X-M).

Since World War II, a group of international organizations (the U.N. the World Bank, IMF, OECD and E.U.) rather than individuals or countries have been setting national accounting standards. Nonetheless, estimating the size and structure of the economy has always been a historically-contingent art — involving political choices — rather than a science. Different methods for measuring “the economy” can produce very different pictures which, in turn, may suggest varied and even contradictory implications for policymakers.

Just look at how financial services are counted in GDP. Until 1993, most measures of economic activity omitted part of FIRE (finance, insurance, and real estate) income. National accountants tended to exclude financial intermediation because they considered the income that financial firms gained by charging interest to be a transfer between various economic sectors. Fee-based financial services (overdrafts, foreign exchange transaction, mergers and acquisitions) were included in GDP as production.

In 1993 even interest-based financial intermediation became defined as productive and entered into GDP calculations. As Brett Christophers explains, the rise of the financial sector in both size and power contributed to changing views about its nature, with the result that the 1993 update of the national accounting standards “made” finance productive by defining it as such, rather than a transfer as before.

Meanwhile the structure of advanced economies changed as well. By 2009 — even after the onset of the financial crisis — FIRE accounted for over a third of all economic activity included in U.S. GDP. Recent years have witnessed a growing divergence between the economic picture painted by GDP on the one hand, and one suggested by employment figures or standard of living measures such as median income, on the other.

The last three recessions in the U.S., for example, have been followed by “jobless recoveries”: GDP rose while unemployment rates remained high and job-creation stagnated, as shown in Figure 1:

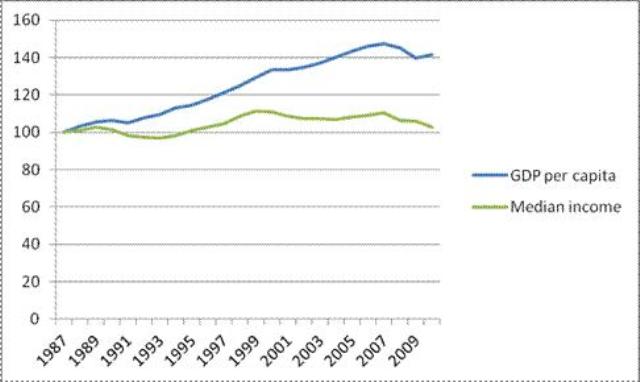

GDP per capita has also diverged dramatically from median income, and thus from the average person’s experience of the economy. As Figure 2 shows, the average standard of living has stagnated since 1987, while standard GDP per capita shows a 47% improvement peaking in 2007.

Does the inclusion of all FIRE revenues in GDP explain these divergences? Popular opinion about the financial sector may wax and wane with the business cycle. Recent research, however, argues that it is always an extractive part of the economy.

At present, as the welfare state recedes and governments step back from providing basic services, people increasingly turn to financial services — mutual funds for retirement, increased debt burdens for education and medical expenses — to meet their family’s needs. This inflates the size of the financial sector, which in turn inflates GDP. But that resulting calculation certainly doesn’t reflect actual economic growth.

Unlike other sectors that produce goods and services, FIRE mostly creates and trades financial assets. In other words, FIRE creates and trades exchange value (money and credit) rather than producing use-value (a good or a service that can be consumed directly). In short, including FIRE in GDP provides an erroneous picture of the amount of goods and services that our economy creates.

Recognizing the error of including all FIRE revenue in GDP calculations also helps to explain why GDP growth in recent years has not translated into job growth, since the employment-creation potential in FIRE is quite limited. Consider a firm managing one billion dollars in assets with 100 staff. If the assets grow tenfold to 10 billion dollars over a year, the firm will not need to hire another 900 employees. In contrast, a car factory or a hair salon would have to increase their payroll quite a lot if blessed with equivalent growth in demand. In fact, finance is the only industry in the U.S. (and in most OECD countries as well) to display a negative correlation between its share of total output and share of total employment. This means either that:

- 1) the FIRE sectors are destroying jobs

- 2) people in finance are super-productive, far beyond the employees of any industry

OR

- 3) Counting finance as adding to GDP is wrong because it does not create any product with use value, but merely trades in exchange value.

What if we put out the FIRE in GDP? What if we treated FIRE revenues as a cost and deducted them from GDP? The resulting adjusted GDP (dubbed Final GDP or FGDP) tracks employment trends far more closely, capturing a better picture of the actual economic growth that citizens experience, rather than growth due mainly to financial accumulation. The finance-as-a-cost version of GDP is also much closer to median income than standard per capita GDP, thus reflecting the average person’s standard of living better. The two graphs below illustrate the improved relevance of FGDP to employment and median income.

If we adjust GDP to account for the costs of finance, two other important implications become clear. First, if we think of FIRE’s fortunes as the price we all pay to produce the rest of GDP, we are better situated to ask questions about how well that sector is doing its job and whether we’ve been overcharged. Secondly, if we think of FIRE as having a negative contribution to GDP, that industry’s greater need for regulation becomes clear.

Once we recognize the hidden assumptions embedded in GDP calculations, our debates over “the economy” moves from a purely ontological level (“how does the economy really behave?”) to a more epistemological one (“how do we know what the economy is?”). National accounting is an art involving historically-specific political choices about what to include or exclude. Adjusting FIRE’s place in our national accounts not only provides a more accurate view of our economy, but one that aligns with progressive goals such as full employment and rising real income for the bulk of the population.