Pro-Palestinian protest encampment at Columbia University (April 22, 2024) | Lev Radin / Shutterstock

The tense stand off on Columbia University campus between student protestors, the university administration, counter-protestors and law enforcement, has become the object of passionate engagement and moral opprobrium across the United States and far beyond. It has sparked movements on campuses across the country and repressive efforts including the deployment of armed police. The issues at stake are Gaza, Israel, the political culture of the United States, norms of behavior and free speech on campus, allegations of anti-semitism, islamophobia and basic issues of control. But at Columbia, at least, the struggle is also about political economy. Indeed, to a surprising degree, questions of political economy are at the heart of the protest. At the same time, it is widely believed that financial anxieties are also influencing the cack-handed response of the university administration.

On Saturday April 20, on a visit to the protest camp on the South Lawn, I was handed this flier.

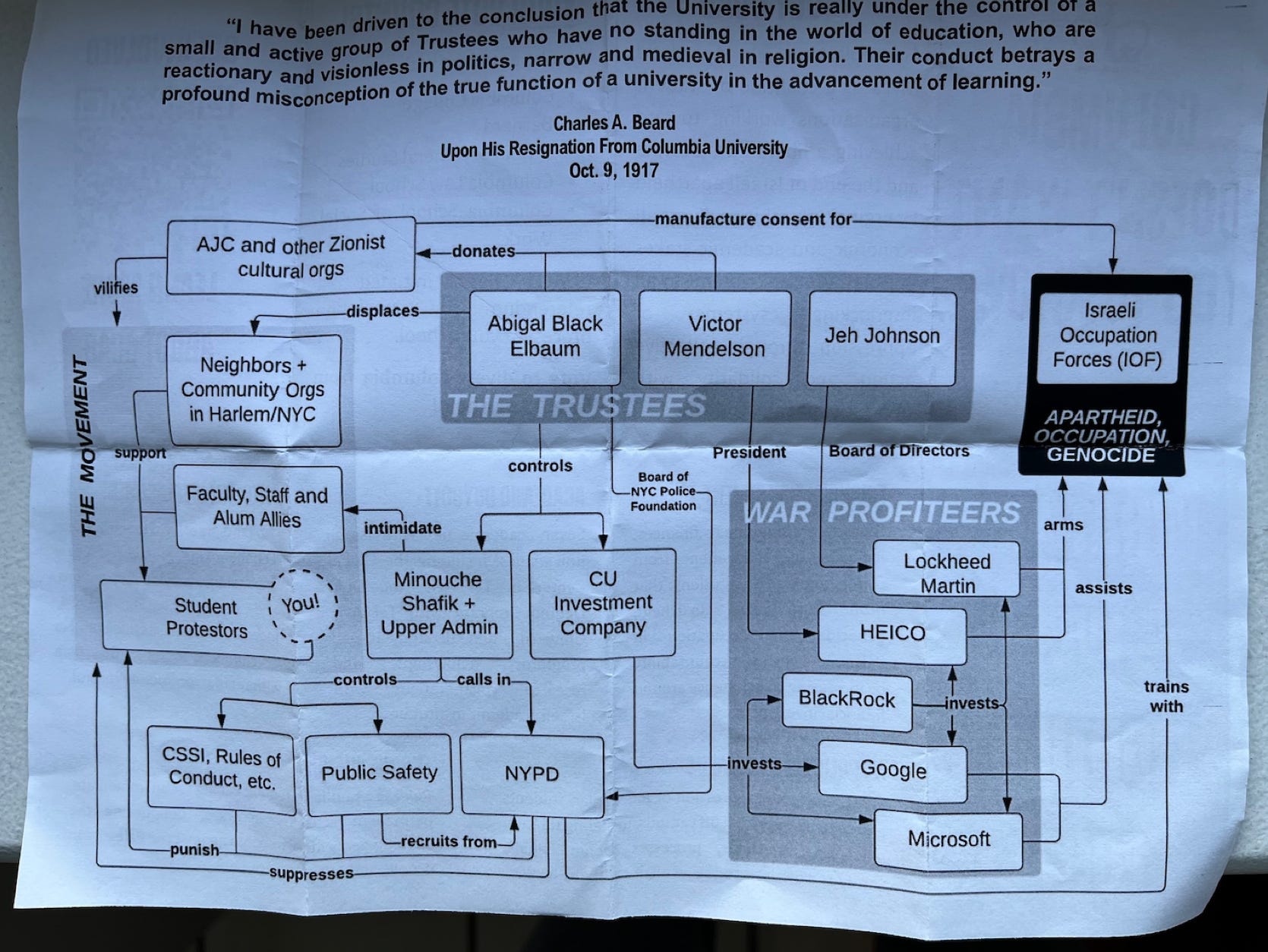

If you open the neatly folded paper square, inside you find this fascinating diagram.

Emblazoned with a stirring quote from Charles A. Beard, the diagram seeks to capture the flow of power in the institution where I have worked since 2015. One of the interesting effects of the diagram is to contextualize some of the figure—notably President Shafik—who have become so central to reportage. Instead, the student analysts seek to focus our attention on corporate power structures and flows of capital and control that spread out beyond the university.

What the flier makes clear is that at least for a substantial part of the protest, the issue at stake is political economy, in the full sense of the word. What they seek to highlight is the way that a powerful educational institution like Columbia is embedded in networks of power and influence, which range from global high finance to the military-industrial complex, “Zionist cultural organizations,” and local real estate development in Manhattan—and specifically Harlem, our immediate neighbor.

The team behind the pamphlet, Columbia University Apartheid Divest, is a coalition of 89 student organizations that claim to represent 3,000 students, a significant fraction of the Columbia student body. CUAD did not come into existence on October 7. It has been mobilizing on campus for some time. CUAD lobbied then-president Bollinger already in 2016. And it does not operate only by means of protests and provocations. It seeks to combine analyses like the one in the flier, with activism and electoral mobilization.

In 2020, CUAD conducted a referendum of the students of Columbia College, in which 61.03 percent of the 1,771 students who participated (1,081) voted in favor of divesting from Israel, 485 voted against, and 205 abstained. In response, university president Lee Bollinger announced the results would not alter Uuniversity investments because “the university should not change its investment policies on the basis of particular views about a complex policy issue, especially when there is no consensus across the university community about that issue.”

A new referendum was proposed by CUAD in March 2024, asking whether the university should divest financially from Israel, cancel the Tel Aviv Global Center, and end Columbia’s dual degree program with Tel Aviv University. The results were released on April 22, after the NYPD, at the invitation of the university leadership, dismantled the first camp and arrested many of its organizers. When the results were reported on April 22, divestment was supported by 76.55 percent of voters, while the latter two propositions garnered 68.36 and 65.62 percent support. The election had 40.26 percent voter participation, with 2,013 students voting, which passed the minimum 30 percent voter participation threshold required by the Columbia College Student Council constitution.

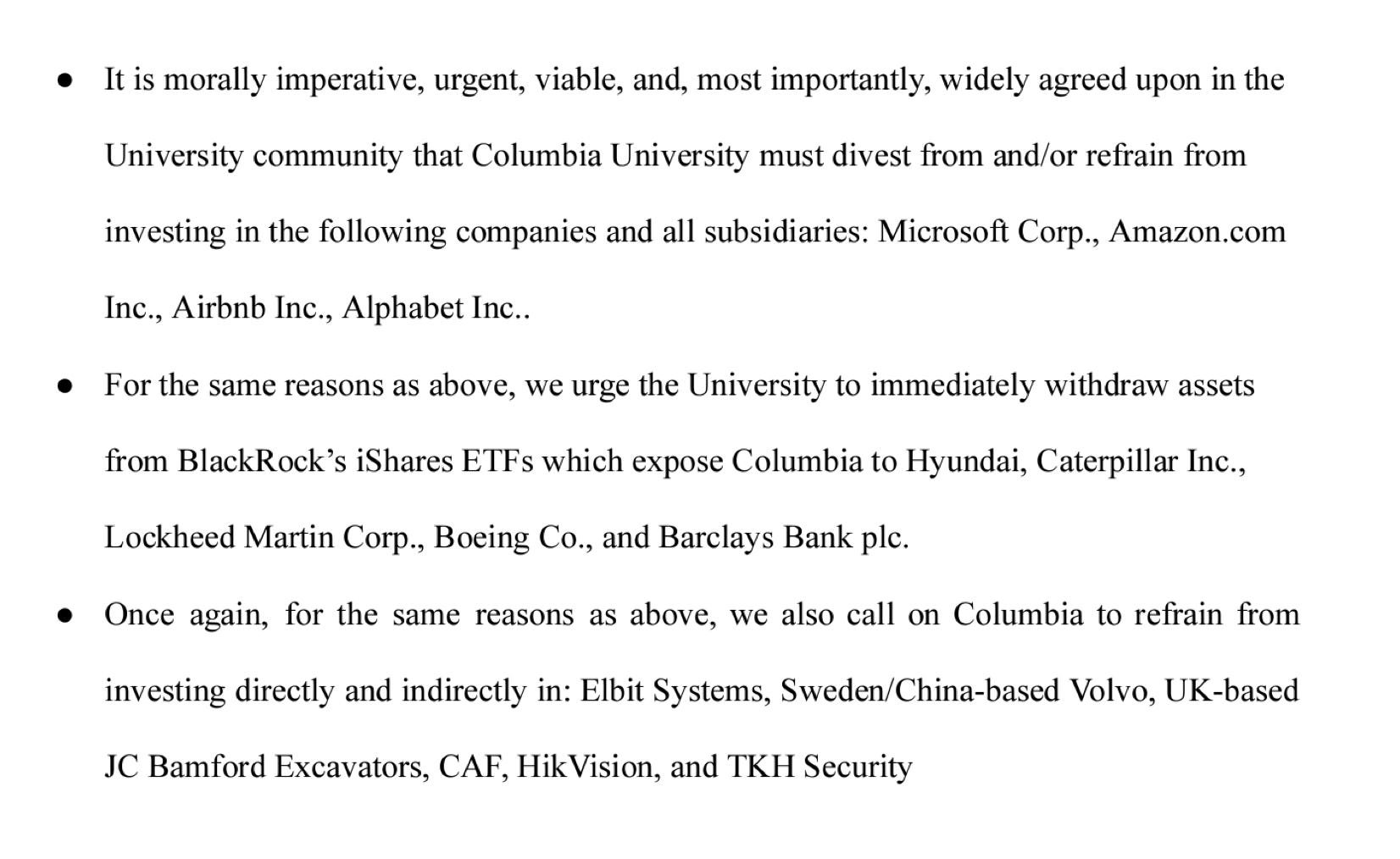

The divestment proposal focuses specifically on publicly traded stocks and bond holdings:

The particular holdings that they target are listed in a spreadsheet. The CUAD proposal was put to the university’s Advisory Committee on Socially Responsible Investing in December 2023. The case was discussed twice by ACSRI, but the particular merits of the divestment proposal were not discussed because ACSRI focused on the question of whether CUAD had established a “broad consensus within the university community regarding the issue at hand.” Ruling that they had not, in February of this year ACSRI rejected the CUAD proposal.

As ACSRI framed it, the issue turned on the definition of Columbia as a community. CUAD used referenda to establish the legitimacy of its demands within Columbia College—what might be called the core undergraduate program on campus. ACSRI’s response was that this was far too narrow a base. ACSRI defines the “Columbia University community” expansively, including not only the huge population of postgraduate students, which takes the student total at Columbia to 36,000 current students, but also 4,600 faculty. Nor did ACSRI stop there. It also insisted that the “Columbia University community” also includes all 385,000 living alumni. For a proposal to pass muster at ACSRI, what is required is not simply a majority but a “broad consensus” across this sprawling network.

To the tightly focused analysis of power and influence mapped by CUAD, the Advisory Committee opposed a definition of Columbia so encompassing and vague as to make the totality impossible to grasp, let alone to mobilize. How could one possibly hope to establish a broad consensus across the more than 420,000 people that ACSRI included in its idea of the “Columbia community”?

Neither definition is innocent. One seeks to lay bare hidden structures of power so as to challenge them. The other cloaks the status quo in an entity so amorphous that it is impossible to see the wood for the trees.

How might we go beyond both these options to produce an encompassing view of Columbia’s political economy that was more inclusive than the CUAD version but not baggy and obfuscating like that offered by ACSRI?

On campus recently, another conflict that has forced self-definition has revolved around unionization. Union activists are concerned to take a holistic view of Columbia, so as to gauge what they may be able to extract in financial concessions. In 2023, CPW-UAW 4100, the Union of Postdoctoral Researchers at Columbia University, and the local chapter of the American Association of University Professors commissioned Professor Howard Bunsis, of Eastern Michigan University, a specialist in the business operations of the American Universities, to make a report on financial condition of Columbia University. His analysis offers us a third take on the question of Columbia’s political economy that can be brought into an illuminating dialogue with the CUAD map.

Bunsis’s conclusions were clear. Though Columbia routinely pleads poverty in denying claims by union organizers, it is, in fact, a truly wealthy organization, which has huge resources and could have even more if it were better managed and less top heavy in its administration. Compared to Columbia’s ample resources, the claims by labor unions were modest and the opposition of the administration to those claims is therefore best understood not in terms of economic trade offs but as an assertion of power. The administration simply does not want to concede the power of employee organizations to make claims on their members behalf.

Bunsis’s analysis is comprehensive, but the first thing he notes is how opaque much of Columbia’s financial reporting is. Bunsis has done similar reports on hundreds of American universities and colleges and he has nothing good to say about Columbia’s accounting. Specifically, compared to other Ivy League colleges, Columbia breaks out its costs far less comprehensively.

Clearly, one demand for that everyone concerned with the future of Columbia should make is for a far greater degree of transparency about what money goes where.

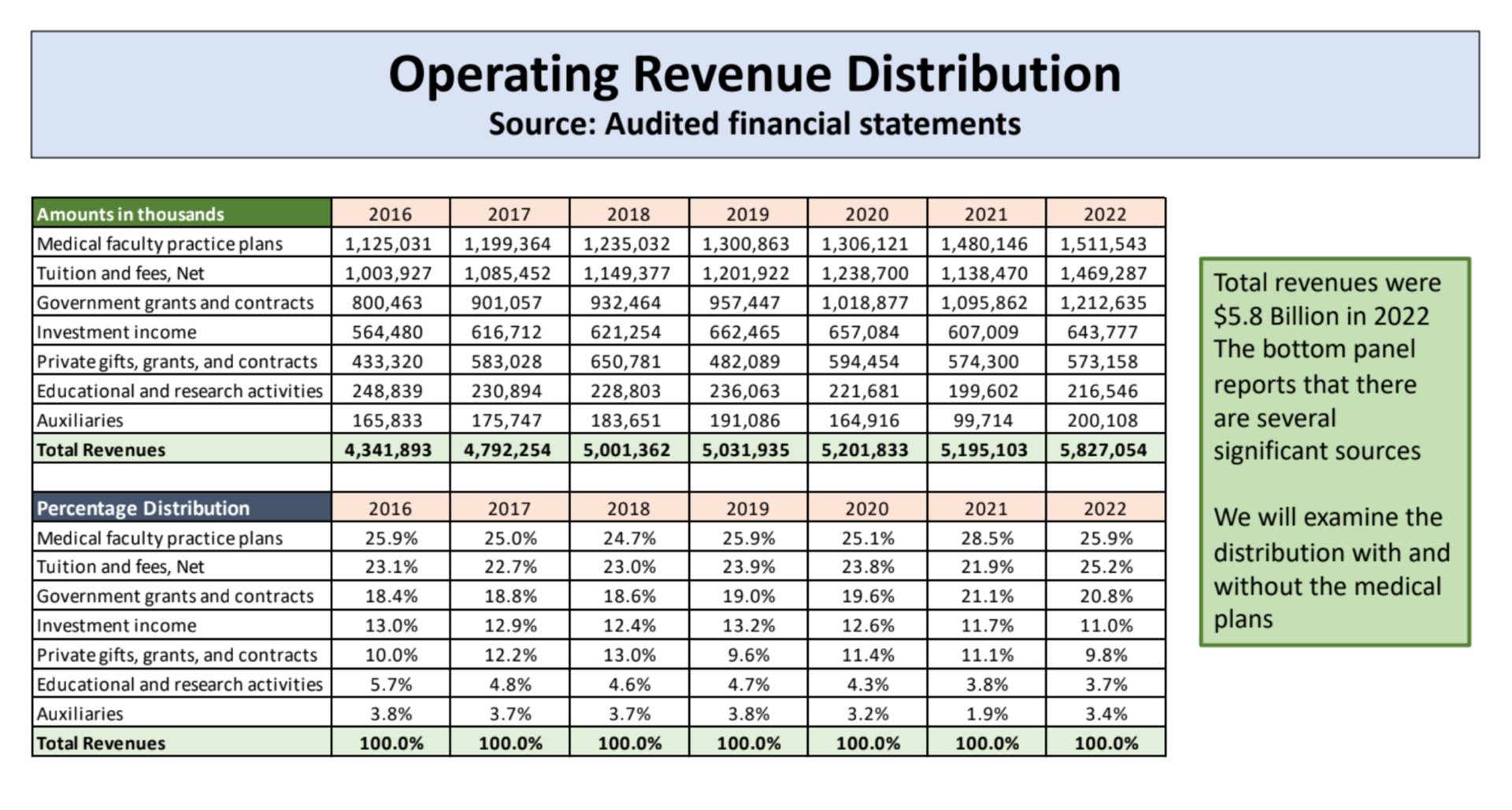

What Columbia does publish is enough to show us that at least in financial and economic terms, Columbia is not one simple thing—an educational institution, or an alumni social network. It is a $5.8 billion-revenue organization consisting of at least seven main entities.

- A medical-industrial complex.

- An externally funded research complex.

- Very large professional schools—business, law, et cetera.

- Columbia College for undergraduates

- A real estate empire—the original core of Columbia’s endowment.

- The fund management organization that manages the financial assets of the endowment.

- A development arm that raises money from alumni.

The relative importance of these seven components can be judged from Bunsis’s table on revenue streams.

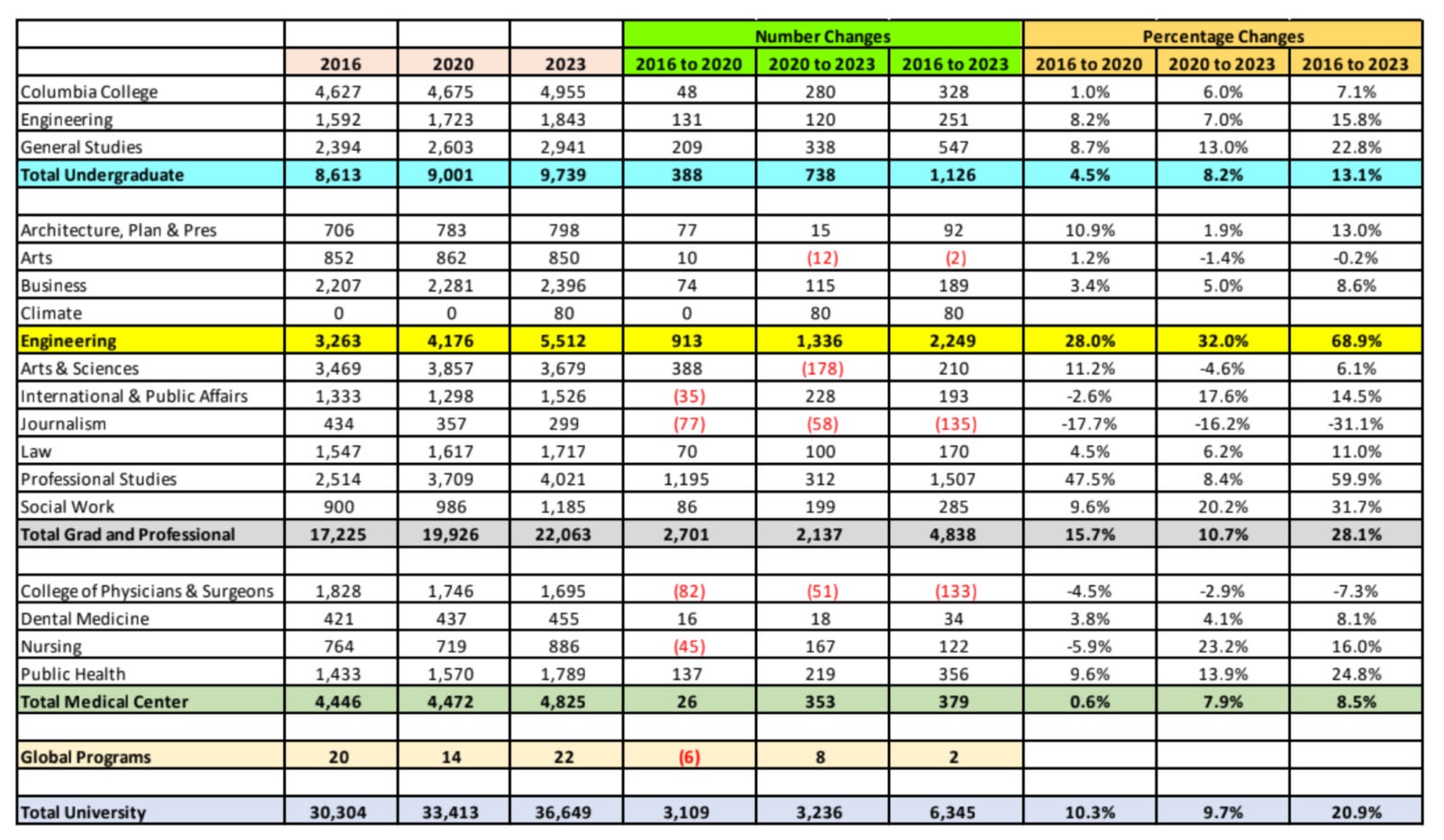

The largest revenue driver is not the educational part of Columbia, but the medical-industrial complex. Tuition net of financial and “discount” at $1.469 billion accounts for 25 percent of revenue. Of the students at Columbia, 27 percent are undergraduates. Columbia college undergrads amongst whom CUAD principally organizes make up 13.5 percent of enrollment in 2023, down from 15.5 percent a few years ago.

All told, tuition revenue from Columbia College undergrads makes up at most 3.25 percent of Columbia University annual revenue, likely less than that considering the higher fees charge in some of the professionals and the heavier ”discount” on undergraduate tuition.

This puts in perspective the dilemma facing the Columbia management but also their disastrous miscalculation of costs and benefits. One can see why management might be impatient with the demands of a few thousand students and perhaps a few hundred graduate students within a much larger university. One can see why they might fear a Congressional attack on over $1.2 billion in grant funding and Federal Pell grants of perhaps $100 million dollars (given to 20 percent of low-income undergrads). But why escalate? Why not defuse what it is a local incident even on Columbia campus? Why risk the “brand value” of degrees being conferred on tens of thousands of other students with a heavy-handed crackdown, vast media attention and further protests? The impulse to coercively impose control on campus in the face of fierce outside criticism has disastrously backfired.

Shafik was clearly under horrible pressure in the Congressional hearings and is no doubt being harangued by threatening voices from all sides. Some of these include the billionaire alumni of Columbia. According to the Forbes Billionaires list, there are at least 19 such people. Their names are: Robert Agostinelli, Louis Bacon, Len Blavatnik, Peter Buck, Warren Buffett, Leon G. Cooperman, Noam Gottesman, Robert Kraft, Henry Kravis, Richard LeFrak & family, Daniel Loeb, David Sainsbury, Thomas Sandell, Shin Dong-Bin, Jerry Speyer, Henry Swieca, S. Robson Walton, Daniel Ziff, Dirk Ziff.

Bob Kraft, the owner of the New England Patriots, has been particularly vocal, suggesting that he would withhold donations. “I am no longer confident that Columbia can protect its students and staff and I am not comfortable supporting the university until corrective action is taken,” he said, in a statement posted on X. Kraft is an alumnus and a longtime donor to Columbia, and he’s also a supporter of Jewish causes: he helped fund the school’s Robert K. Kraft Center for Jewish Student Life and started the Foundation to Combat Antisemitism. Already in November last year, Henry Swieca resigned from the Business School board.

Cooperman, Blavatnik, and Kraft are credited with donations worth nearly $100 million to Columbia. This is a lot of money. But in light of Columbia’s endowment, which runs close to $15 billion, it is hard to see why such a contribution, split between three donors over many years, should move the dial. The fear no doubt is that where Kraft leads others may follow. Perhaps more ominous are trends in the school’s “annual fund,” which covers the cost of scholarships, student life and internships, and where participation among donors may be down by 25 percent to 30 percent this year.

The extraordinary data combined by the Altrata group allow us to gauge how big is the donor pool beyond the billionaire elite.

The top 20 US universities churning out the most ultra-wealthy alums (net worth in excess of $30) million:

- 1.Harvard University 17,660

- 2.Stanford University 7,972

- 3.University of Pennsylvania 7,517

- 4.Columbia University 5,528

- 5.New York University 5,214

Altrata also compiles data on business leaders and their uUniversity affiliations, again Columbia has a big network and much to lose. If these data are to be believed, approximately 2.3 percent of all senior executives in the United States appear to have some Columbia connection. With 1,557 alumni serving as senior executives in major global companies Columbia comes in fourth place, behind Harvard with 3,879, Penn with 2,387, and Stanford with 2,017.

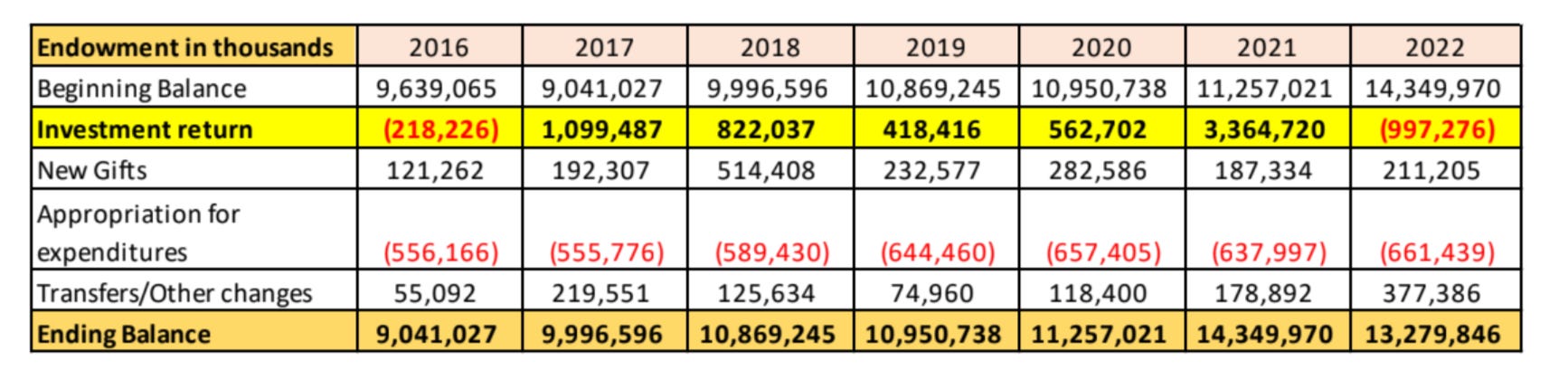

So, fundraising and development concerns may be driving the administration’s efforts to silence the protests. But when one looks at the accounting data, it is not obvious why this should be the priority that it is often taken to be. Investment returns on the existing financial endowment are generally speaking far more significant than the relatively modest flow of new gifts.

The imbalance would be even greater if Columbia actually achieved a better rate of return on its endowment. Since 2016, the rate of return has been remarkably poor. In every single year since 2016, Columbia’s endowment has underperformed the S&P500.

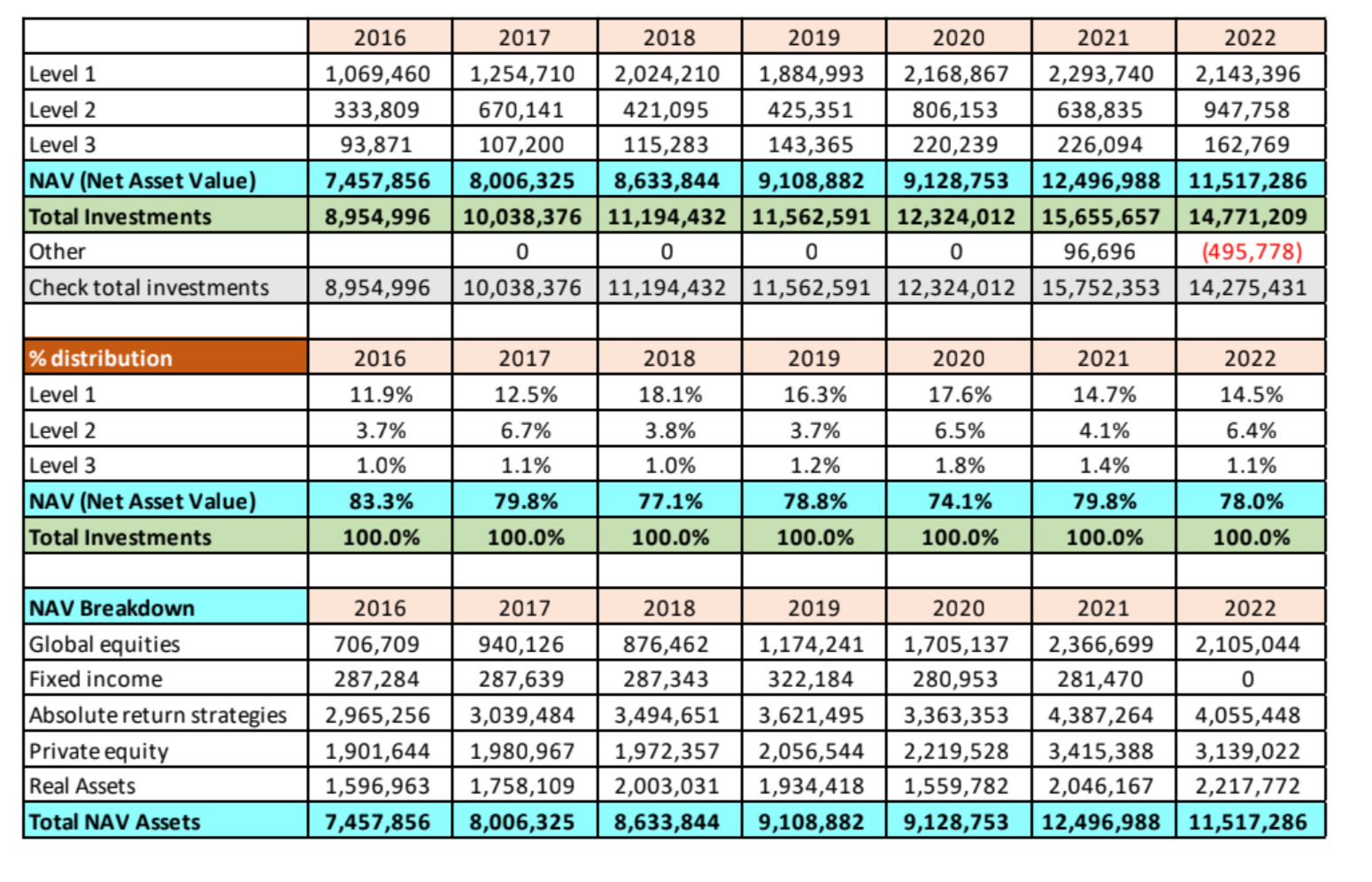

If Columbia had simply put its money in a widely based index fund it could have achieved its current endowment level, and more, without attracting a single cent in new donations from alumni and other donors. How, you might ask, can a fund as large as Columbia’s manage to underperform the S&P500 index so badly? The answer is that most of Columbia’s money is not, in fact, invested in public markets.

Columbia is a victim of the hype around alternative investments, private equity, hedge funds, and the like. And yet, for lack of any more public information about Columbia’s endowment allocation, it is precisely on the minority of funds that are invested in publicly traded assets and exchange traded funds that the student activists are forced to concentrate their fire. And the assets that they would like to see divested are correspondingly tiny. A few millions here or there in relation to an endowment of almost $15 billion.

So, from the point of view political economy, the whole dispute has the feel of shadow boxing. A small group of students camped on one lawn, in a very large university complex, calling for relatively minor financial rearrangements in a baggy and poorly managed endowment, are turned by the repressive action of the university administration under pressure from politicians and donors, into a global news story, putting in doubt the standing of a multi-billion dollar educational, research, and medical organization. It is a case study in panicked control-freakery gone wrong. If the cause that the students are protesting were not so serious, if the slander heaped on them were not so manifestly unjust, the whole affair would have the feel of a dark comedy. One thinks of that 1980s New York classic, Tom Wolfe’s Bonfire of the Vanities.

No doubt experts in university finances will find the treatment I have given here simplistic. They will call into question the complacent analysis of Columbia’s riches and question whether the management really has the scope for independent judgement and action that I am implying. There are no doubt complex issues of budget management and fund allocation. Columbia is not one big well-organized corporation that the accounts paint it as. It is split into many fiefdoms, each with their own financial accounts and constraints. And yet, in the end, a summative financial judgement on its underlying position and the freedom of action this implies, is not merely an abstract exercise. There are agencies divorced from campus politics that make precisely such assessments all the time. And tens of billions of dollars of debt depend on those judgements. I am talking about the ratings agencies that evaluate the bonds issued by issued by America’s universities.

As the graphic makes clear, the judgement of Moody’s on Columbia’s financial situation is resounding. Columbia is not just investment grade. It is squarely situated in the top tier of American universities that issue debt that is triple-A rated. Very few private debt issuers enjoy such a high standing. As Moody’s makes clear, that rating depends on a comprehensive assessment of Columbia’s balance between revenue flow and costs. That calculation includes its relations with alumni and donors. If Moody’s issues a downgrade warning, Columbia would be miles away from serious financial stress, but it would mean that the current crisis had entered a new stage of seriousness.

This essay was first published in Chartbook, the author’s Substack, on April 26, 2024. Reprinted with permission.

One thought on “Columbia University’s “Crisis””